In the field of economics, the term equilibrium price plays a central role in understanding how markets function. It refers to the price at which the quantity of a good demanded by consumers equals the quantity supplied by producers. This point of balance is crucial for understanding market efficiency, resource allocation, and the overall functioning of a free market economy.

The equilibrium price is influenced by a number of factors, including demand and supply, and it provides valuable insights into how changes in these factors can affect the price level and quantity of goods exchanged in the market. In this article, we will explore the concept of equilibrium price in detail, examining its definition, the factors that determine it, and how it impacts the market.

Definition of Equilibrium Price

The equilibrium price is the price at which the quantity of a good or service demanded by consumers is equal to the quantity that producers are willing to supply. It is also referred to as the “market-clearing price” because at this price, there is neither a surplus nor a shortage of the good in question. In other words, the amount of the good that buyers want to purchase exactly matches the amount that sellers want to sell.

At the equilibrium price, there is no upward or downward pressure on the price, meaning that market forces of supply and demand are balanced. This price ensures that all goods are sold, and every consumer who wants to purchase the good at that price can do so.

The Role of Demand and Supply in Determining Equilibrium Price

To better understand the equilibrium price, it’s essential to look at the two fundamental forces that drive the market: demand and supply.

Demand and Its Impact on Price

Demand refers to the quantity of a good or service that consumers are willing and able to purchase at different price levels. Generally, as the price of a good decreases, the quantity demanded increases, and as the price increases, the quantity demanded decreases. This inverse relationship between price and demand is known as the law of demand.

When the price of a product is lower, consumers are more willing to buy it because they perceive it as more affordable. Conversely, when the price is higher, fewer consumers will be willing to purchase the good.

Supply and Its Impact on Price

Supply, on the other hand, refers to the quantity of a good or service that producers are willing and able to offer for sale at different price levels. The law of supply states that, all other factors being equal, as the price of a good increases, the quantity supplied increases as well. This is because producers are more motivated to supply more of a good when they can sell it at a higher price.

If the price of a product is low, producers may not find it profitable to supply large quantities, and may choose to decrease production. On the other hand, if the price is high, producers are incentivized to increase supply to capitalize on the higher profit margins.

How Supply and Demand Interact to Determine Equilibrium Price

The equilibrium price is the point where the demand and supply curves intersect. At this price, the quantity demanded by consumers is equal to the quantity supplied by producers. There is no surplus or shortage of goods, and the market is in balance.

When the market price is above the equilibrium price, the quantity supplied exceeds the quantity demanded, resulting in a surplus. Producers may lower the price to clear the excess goods, pushing the price back down toward the equilibrium point.

Conversely, when the market price is below the equilibrium price, the quantity demanded exceeds the quantity supplied, creating a shortage. Consumers may be willing to pay more for the product, which incentivizes producers to raise the price, thus restoring balance in the market.

Shifts in Supply and Demand

It is important to note that the equilibrium price is not static. It can change if either the demand or supply curve shifts. Factors such as changes in consumer preferences, income levels, production costs, or the introduction of new technologies can all influence supply and demand.

Demand Shifts

An increase in demand shifts the demand curve to the right, which typically results in a higher equilibrium price and higher quantity. Conversely, a decrease in demand shifts the demand curve to the left, leading to a lower equilibrium price and lower quantity.

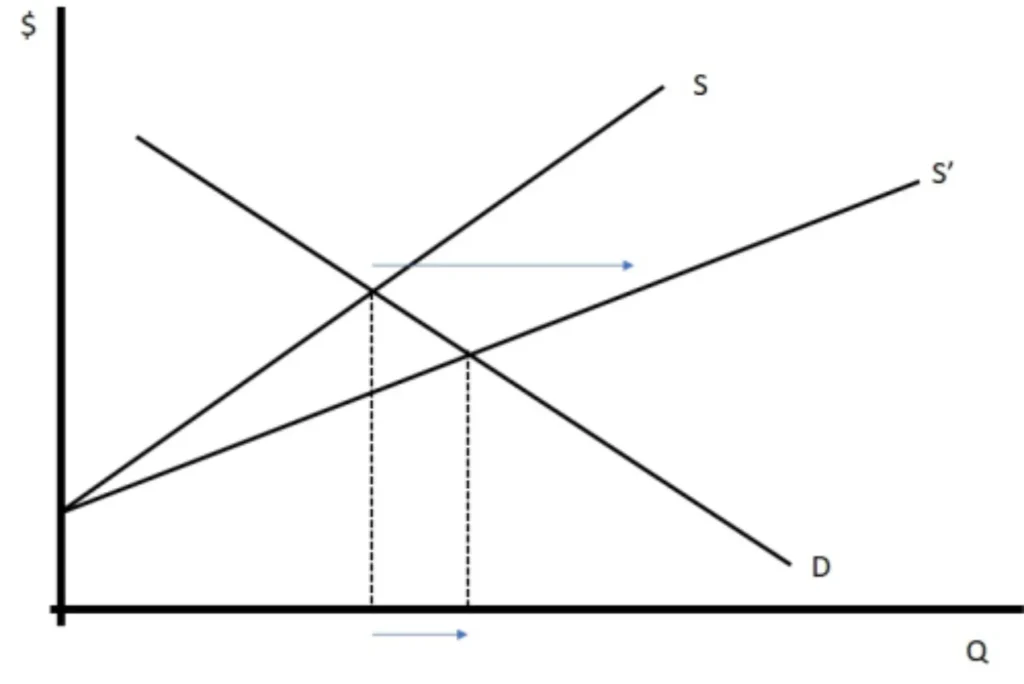

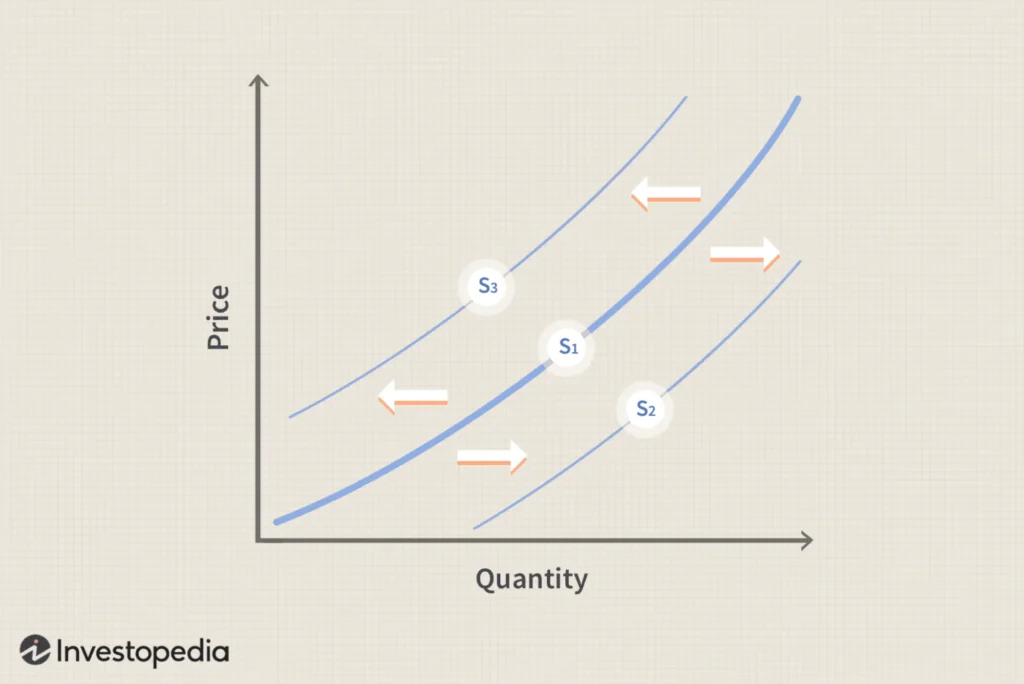

Supply Shifts

An increase in supply shifts the supply curve to the right, leading to a lower equilibrium price and higher quantity. A decrease in supply shifts the supply curve to the left, resulting in a higher equilibrium price and lower quantity.

Factors That Influence the Equilibrium Price

Several external factors can cause shifts in demand or supply, thereby impacting the equilibrium price. Some of the key factors include:

Consumer Preferences

A change in consumer preferences can lead to a shift in the demand curve. For example, if a product becomes more fashionable or desirable, the demand for it will increase, raising the equilibrium price.

Income Levels

An increase in consumer income can lead to higher demand for goods and services, particularly for normal goods. This shift in demand results in a higher equilibrium price.

Production Costs

Changes in the cost of production, such as labor costs, raw materials, or energy, can affect the supply curve. An increase in production costs may decrease the supply of a good, leading to a higher equilibrium price.

Technological Advancements

New technologies can improve production efficiency, shifting the supply curve to the right. This results in a lower equilibrium price and a greater quantity of goods being supplied.

Government Policies

Taxes, subsidies, price controls, and regulations can all influence the equilibrium price. For example, a government subsidy to producers may increase the supply of a good, reducing its equilibrium price.

External Shocks

Events such as natural disasters, geopolitical crises, or pandemics can disrupt both demand and supply, leading to changes in the equilibrium price. For example, a pandemic might reduce consumer spending, shifting the demand curve to the left and lowering the equilibrium price.

Equilibrium Price in Real-World Markets

While the theoretical concept of equilibrium price is essential for understanding how markets function, real-world markets often experience fluctuations that prevent prices from reaching perfect equilibrium. However, even in these cases, prices generally adjust over time as supply and demand interact.

In practice, the equilibrium price is a moving target. For example, during the holiday season, the demand for certain products may increase, pushing prices above their usual equilibrium levels. In response, producers may increase supply to meet the heightened demand, and over time, prices may return to a more balanced level.

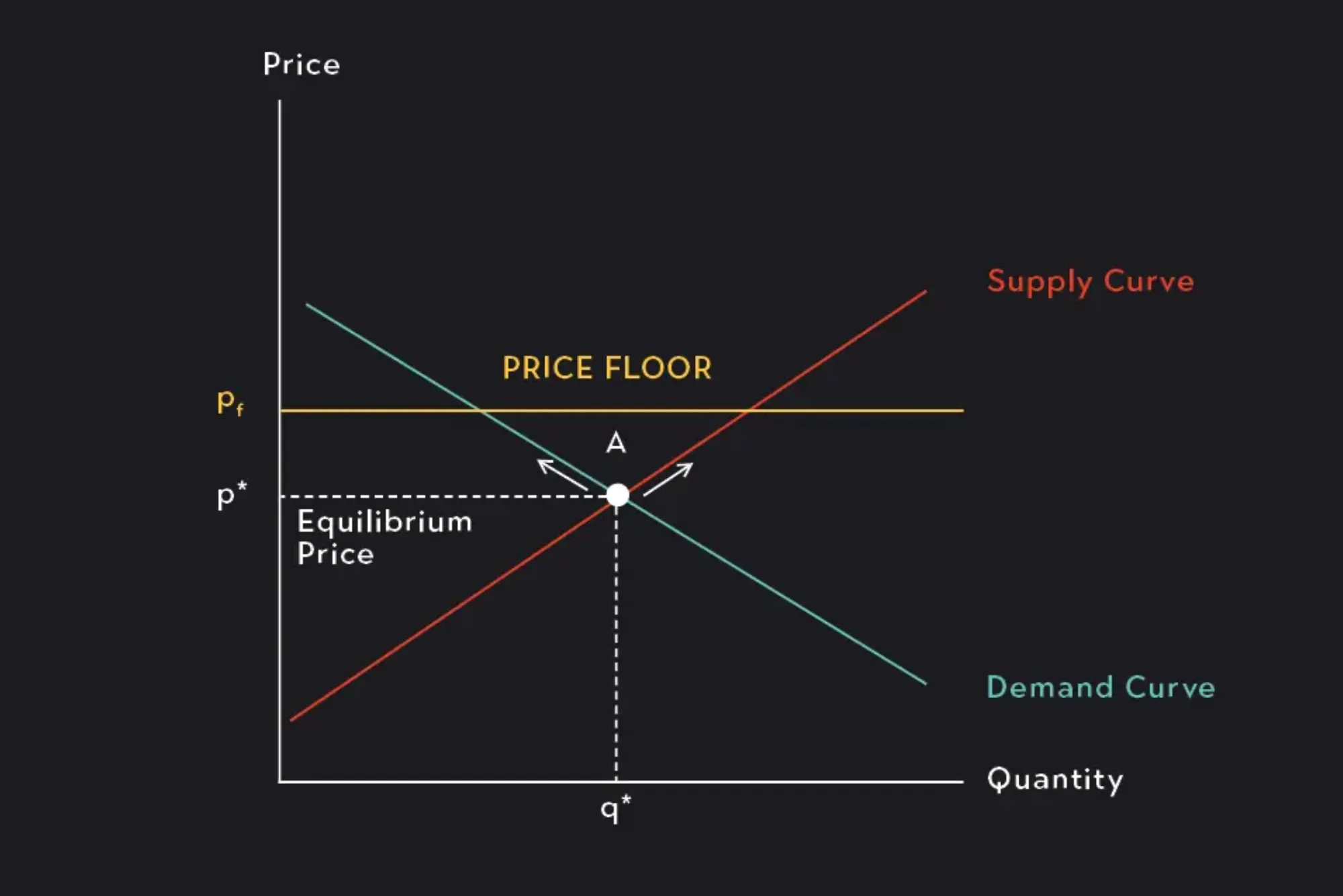

Additionally, government interventions, such as price floors and price ceilings, can distort the natural equilibrium. A price floor, such as a minimum wage, sets a minimum price for a good or service, which may create a surplus if the price is too high. A price ceiling, such as rent control, sets a maximum price, which can lead to shortages if the price is too low.

The equilibrium price is a fundamental concept in economics that illustrates the balance between supply and demand in a market. It represents the price at which the quantity of a good demanded by consumers equals the quantity supplied by producers, ensuring that the market clears without any shortages or surpluses.